What are Amortization and Depreciation? What are the Differences?

Mar 16, 2024 By Triston Martin

The techniques of depreciation and amortization are used to calculate how much the cost of intangible as well as tangible resources has decreased or increased over a given time period. It is crucial to comprehend these two accounting principles while purchasing real estate or investing in assets connected to your business.

Understanding the distinctions between these concepts might enable you to make more cost-effective and time-efficient financial decisions. This article defines amortization and depreciation, explains their distinctions, and gives examples of both accounting techniques.

What is Amortization?

The accounting technique of spreading an intangible asset's cost over the course of its useful life is called amortization. Despite not being real, intangible assets nonetheless have value. Franchise agreements, copyrights, trademarks, patents, expenditures associated with issuing bonds to raise money, and organizational expenses are a few examples of intangible belongings that have been expensed through amortization.

Usually, amortization is expensed using a straight-line method. This indicates that during the asset's useful life, the same value is expensed every quarter. Generally, objects that are deductible using the amortization approach are not valuable for salvage or resale. There is another separate circumstance in which the term amortization is employed.

When calculating a series of installments for a loan that, such in the example of a mortgage, includes principle as well as curiosity in each installment, an amortization schedule is frequently utilized. Despite being distinct, the idea is rather similar. Since a loan is a type of intangible asset, amortization is the process of lowering the balance's carrying value.

What is Depreciation?

The expense of an investment that is fixed throughout its useful life is known as depreciation. A business's fixed assets are actual items that it has purchased. Commonly depreciated permanent or physical assets include buildings, machinery, office furniture, cars, and equipment. In contrast to intangible wealth, tangible assets could still be valuable when the company no longer needs them. Because of this, the asset's salvage or resale value is subtracted from its initial cost to determine depreciation.

The difference is equally depreciated throughout the asset's anticipated life in years. Put otherwise, the corporation may deduct the reduced amount expensed each year from its taxes up until the asset's useful life ends. For instance, a company may construct or purchase an office building and occupy it for a number of years. After that, the company moved to a larger, newer facility in a different location. Despite its state of disrepair, the old office block is still worth something.

A portion of the building's cost is expensed for each accounting year, and the remaining balance is spread out throughout the structure's anticipated life, less its resale value. Certain fixed assets might have their depreciation done on an advanced basis, which means that a bigger percentage of the asset's market value is written off in the initial years of the asset's life. Usually, vehicles experience increased depreciation.

Comparing Amortization Costs with Depreciation Costs

Amortization expenditure is the term for the writing away of an intangible resource over the course of its useful life. The quantity of an amortization expense write-off is often shown in the income statement's "depreciation and amortization" line item.

A debit to the amortisation expenditure account together with a credit to the cumulative amortisation account represent the accounting for amortisation expense. The cumulative amortization account is often linked to the intangible property line item and appears on the statement of financial position as a contra account, which balances the amount in a related account. The same idea holds true for depreciation expenditure, which is billed as an expense that is not in cash and represents a portion of a fixed investment that has been deemed spent in the current quarter.

To balance the credit added to the accumulation of depreciation account, a contribution is made to the expense for depreciation account. A counter asset account is a cumulative depreciation account that balances the fixed assets account. The sum in the depreciation expenditure account, which rises during the client's fiscal year, is cancelled off inside of the year-end close. The account is again utilised to hold depreciation costs for the next fiscal year.

Advantages of Depreciation and Amortization

For business clients, amortization and depreciation may be quite advantageous because they are both tax deductible as business costs. They can be particularly advantageous for smaller companies with tighter financial constraints.

Amortisation has several advantages, one of which is the ability to reduce a client's tax liability for the fiscal year in question for as lengthy as the asset remains in use. Additionally, a customer can utilize amortization to lower their taxes in years when they reach a higher tax rate if they anticipate having a larger income in the future.

Depreciating assets helps businesses pay less in taxes. Additionally, depreciating an asset's value throughout its lifespan of use and calculating it as an expenditure helps businesses better align asset uses with benefits as they are unable to charge an asset in a single period. Additionally, it facilitates asset appraisal, allowing customers to report assets at their net book value with greater accuracy. Form 4562 needs to be submitted with the client's yearly tax return in order to claim degradation and amortization deductions.

Amortization vs. Depreciation Example

Amazon (AMZN) provided full-year comparison financial statements with financial statement notes in its 2021 annual report. According to the firm's cash flow statement, Amazon combined depreciation and amortization, reporting a total of $34,296 in activity. Amazon provided an explanation of its depreciation and amortization policies, as is customary in financial statement disclosures. The business employs the straight-line approach for both. However, depending on the actual asset, it employs a broad variety of usable lifetimes.

The Bottom Line!

To reflect an asset's benefit and related expenses over time, two popular methods are employed. Both amortization and depreciation lower an asset's carrying value and acknowledge costs as they are incurred throughout the course of asset usage.

On the other hand, intangible assets are amortized, while physical assets are depreciated. Furthermore, there exist variations in the approaches that can be employed, choices for acceleration, the application of salvage value, and the utilisation of contra accounts.

-

Banking Dec 18, 2023

Banking Dec 18, 2023Simplifying Real Estate: A Deep Dive Into How a 1031 Exchange Works

Dive into the world of real estate investment with our comprehensive guide on 1031 Exchange. Learn its workings, benefits, and potential pitfalls to maximize returns.

-

Taxes Mar 16, 2024

Taxes Mar 16, 2024Simple Guide to Record the Lease Liability and Corresponding Asset

Let’s understand the complexities of recording lease liability and assets with ease. Our simple guide breaks down the process, ensuring accuracy and compliance.

-

Taxes Mar 15, 2024

Taxes Mar 15, 2024Money-Saving Mania: The Ultimate Guide to Energy Efficient Tax Credits

Ready to save some serious cash and help the planet? Our ultimate guide to energy-efficient tax credits will make you feel like a green superhero in no time.

-

Know-how Jan 08, 2024

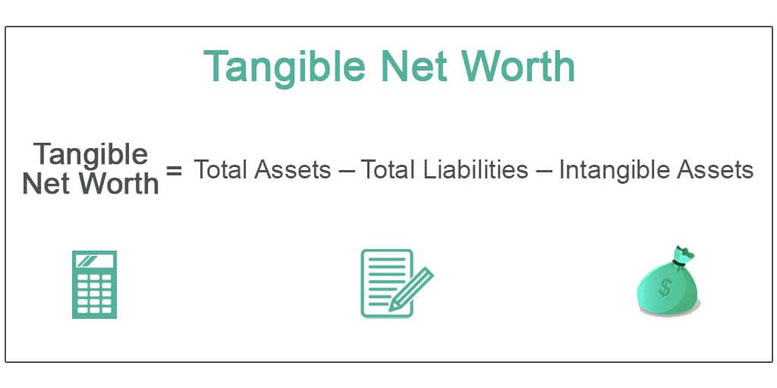

Know-how Jan 08, 2024A Quick Guide: How to Calculate Your Tangible Net Worth?

When calculating net worth, it is necessary to consider all possible debts and deduct them from the value of the assets. Despite the apparent ease of the procedure, the major challenge here is determining the maximum value of all potential assets and liabilities. This challenge might be exacerbated by a lack of or incorrect understanding of basic financial principles.